Jackals of Jekyll Island – Federal Reserve Audit

The supreme illicit fraud of central banking embodied in the Federal Reserve, acts as a private piggybank for favored cartel thieves. The liquidity of unlimited credit transfers to banksters, especially at zero interest, financed by unimaginable new Treasury Bonds, indebting the American public; is a crime committed by outlaws. The significance of the evidence for the extent of the crony financial manipulations, that the controllers of international capital use to maintain their power strangle hold on humanity, needs to be fully exposed. Only when the beleaguered and downtrodden become sufficiently indignant to usury incarceration, will heads start to roll.

“The first top-to-bottom audit of the Federal Reserve uncovered eye-popping new details about how the U.S. provided a whopping $16 trillion in secret loans to bail out American and foreign banks and businesses during the worst economic crisis since the Great Depression. An amendment by Sen. Bernie Sanders to the Wall Street reform law passed one year ago this week directed the Government Accountability Office to conduct the study. “As a result of this audit, we now know that the Federal Reserve provided more than $16 trillion in total financial assistance to some of the largest financial institutions and corporations in the United States and throughout the world,” said Sanders. “This is a clear case of socialism for the rich and rugged, you’re-on-your-own individualism for everyone else.”

Yes, you read that correct, 16 TRILLION DOLLARS. When originally disclosed, there was minimal outrage.

“The FOMC approved these swap line arrangements to help address challenges in the global market for interbank lending in U.S. dollars. Many foreign banks held U.S. dollar-denominated assets and faced challenges borrowing in dollars to fund these assets. In contrast to U.S. commercial banks, foreign banks did not hold significant U.S. dollar deposits, and as a result, dollar funding strains were particularly acute for many foreign banks. The Board of Governors of the Federal Reserve System (Federal Reserve Board) staff memos recommending that the FOMC approve swap lines noted that continuing strains in dollar funding markets abroad could further exacerbate strains in U.S. funding markets. For example, foreign banks facing difficulties borrowing against U.S. dollar assets may have faced increased pressure to sell these assets at a time of stress, potentially putting downward pressure on prices for these assets. The dollar swap lines allowed foreign central banks to make dollar loans to banks in their jurisdictions without being forced to draw down dollar holdings of foreign exchange reserves or to acquire dollars directly in the foreign exchange market. An FRBNY staff paper noted that the dollar reserves of many foreign central banks at the start of the crisis were smaller than the amounts they borrowed under the swap lines and that efforts by foreign central banks to buy dollars in the market could have crowded out private transactions, making it more difficult for foreign banks to obtain dollars. This paper further noted that the Federal Reserve System (the Federal Reserve Board and Reserve Banks collectively) was in a unique position to provide dollars needed by foreign central banks to provide lender-of-last-resort liquidity to banks in their jurisdictions. The increase in reserves was offset through sales of Treasury securities and increasing incentives for depository institutions to hold excess reserves at FRBNY.”

“Another mystery that I would like to see addressed is the trillions of dollars of “off balance sheet transactions” that are unaccounted for at the Federal Reserve. This was brought up once during a Congressional hearing, but nobody seemed to have any answers.”

The $9,000,000,000,000 MISSING From The Federal Reserve YouTube captures the absurdity of Congressional oversight. The financial community that created fractional reserve banking is in total control of the political election process. As long as there is no accountability and consequences for outright theft, the money magicians continue to operate their fraudulent scheme of deception as the cornerstone of international economic transactions.

The FED’s grip on the global moneychangers’ racket is based upon maintaining the U.S. Federal Reserve funny money, as the reserve currency for the planet. The value and worth of Treasury Bills and Bonds are on the path to have the value of Reichsbank marks. Recognize the enemy that is destroying the country and world economy

| Here is a candidate for president. "We don't need to waste more money on a Commission." Spend let's say $30,000,000 at the most on $16,000,000,000,000? I guess that is too much to investigate on! Let's pay ourselves to the Bankers, because they love us, the Federal Reserve is of course Government-owned, if you say anything else, you are a crazy Conspiracy Theorist that hates freedom and liberty... Herman Cain is exposed as an operative. “ |

– The Honorable Louis McFadden, Chairman of the House Banking and Currency Committee in the 1930s The Federal Reserve (or Fed) has assumed sweeping new powers in the last year. In an unprecedented move in March 2008, the New York Fed advanced the funds for JPMorgan Chase Bank to buy investment bank Bear Stearns for pennies on the dollar. The deal was particularly controversial because Jamie Dimon, CEO of JPMorgan, sits on the board of the New York Fed and participated in the secret weekend negotiations.1 In September 2008, the Federal Reserve did something even more unprecedented, when it bought the world’s largest insurance company. The Fed announced on September 16 that it was giving an $85 billion loan to American International Group (AIG) for a nearly 80% stake in the mega-insurer. The Associated Press called it a "government takeover," but this was no ordinary nationalization. Unlike the U.S. Treasury, which took over Fannie Mae and Freddie Mac the week before, the Fed is not a government-owned agency. Also unprecedented was the way the deal was funded. The Associated Press reported: "The Treasury Department, for the first time in its history, said it would begin selling bonds for the Federal Reserve in an effort to help the central bank deal with its unprecedented borrowing needs."2 This is extraordinary. Why is the Treasury issuing U.S. government bonds (or debt) to fund the Fed, which is itself supposedly "the lender of last resort" created to fund the banks and the federal government? Yahoo Finance reported on September 17: "The Treasury is setting up a temporary financing program at the Fed’s request. The program will auction Treasury bills to raise cash for the Fed’s use. The initiative aims to help the Fed manage its balance sheet following its efforts to enhance its liquidity facilities over the previous few quarters." Normally, the Fed swaps green pieces of paper called Federal Reserve Notes for pink pieces of paper called U.S. bonds (the federal government’s I.O.U.s), in order to provide Congress with the dollars it cannot raise through taxes. Now, it seems, the government is issuing bonds, not for its own use, but for the use of the Fed! Perhaps the plan is to swap them with the banks’ dodgy derivatives collateral directly, without actually putting them up for sale to outside buyers. According to Wikipedia (which translates Fedspeak into somewhat clearer terms than the Fed’s own website): "The Term Securities Lending Facility is a 28-day facility that will offer Treasury general collateral to the Federal Reserve Bank of New York’s primary dealers in exchange for other program-eligible collateral. It is intended to promote liquidity in the financing markets for Treasury and other collateral and thus to foster the functioning of financial markets more generally. . . . The resource allows dealers to switch debt that is less liquid for U.S. government securities that are easily tradable." "To switch debt that is less liquid for U.S. government securities that are easily tradable" means that the government gets the banks’ toxic derivative debt, and the banks get the government’s triple-A securities. Unlike the risky derivative debt, federal securities are considered "risk-free" for purposes of determining capital requirements, allowing the banks to improve their capital position so they can make new loans. (See E. Brown, "Bailout Bedlam," webofdebt.com/articles, October 2, 2008.) In its latest power play, on October 3, 2008, the Fed acquired the ability to pay interest to its member banks on the reserves the banks maintain at the Fed. Reuters reported on October 3: "The U.S. Federal Reserve gained a key tactical tool from the $700 billion financial rescue package signed into law on Friday that will help it channel funds into parched credit markets. Tucked into the 451-page bill is a provision that lets the Fed pay interest on the reserves banks are required to hold at the central bank."3 If the Fed’s money comes ultimately from the taxpayers, that means we the taxpayers are paying interest to the banks on the banks’ own reserves – reserves maintained for their own private profit. These increasingly controversial encroachments on the public purse warrant a closer look at the central banking scheme itself. Who owns the Federal Reserve, who actually controls it, where does it get its money, and whose interests is it serving?

Not Private and Not for Profit?

The Fed’s website insists that it is not a private corporation, is not operated for profit, and is not funded by Congress. But is that true? The Federal Reserve was set up in 1913 as a "lender of last resort" to backstop bank runs, following a particularly bad bank panic in 1907. The Fed’s mandate was then and continues to be to keep the private banking system intact; and that means keeping intact the system’s most valuable asset, a monopoly on creating the national money supply. Except for coins, every dollar in circulation is now created privately as a debt to the Federal Reserve or the banking system it heads.4 The Fed’s website attempts to gloss over its role as chief defender and protector of this private banking club, but let’s take a closer look. The website states: * "The twelve regional Federal Reserve Banks, which were established by Congress as the operating arms of the nation’s central banking system, are organized much like private corporations – possibly leading to some confusion about "ownership." For example, the Reserve Banks issue shares of stock to member banks. However, owning Reserve Bank stock is quite different from owning stock in a private company. The Reserve Banks are not operated for profit, and ownership of a certain amount of stock is, by law, a condition of membership in the System. The stock may not be sold, traded, or pledged as security for a loan; dividends are, by law, 6 percent per year." * "[The Federal Reserve] is considered an independent central bank because its decisions do not have to be ratified by the President or anyone else in the executive or legislative branch of government, it does not receive funding appropriated by Congress, and the terms of the members of the Board of Governors span multiple presidential and congressional terms." * "The Federal Reserve’s income is derived primarily from the interest on U.S. government securities that it has acquired through open market operations. . . . After paying its expenses, the Federal Reserve turns the rest of its earnings over to the U.S. Treasury."5 So let’s review: 1. The Fed is privately owned. Its shareholders are private banks. In fact, 100% of its shareholders are private banks. None of its stock is owned by the government. 2. The fact that the Fed does not get "appropriations" from Congress basically means that it gets its money from Congress without congressional approval, by engaging in "open market operations." Here is how it works: When the government is short of funds, the Treasury issues bonds and delivers them to bond dealers, which auction them off. When the Fed wants to "expand the money supply" (create money), it steps in and buys bonds from these dealers with newly-issued dollars acquired by the Fed for the cost of writing them into an account on a computer screen. These maneuvers are called "open market operations" because the Fed buys the bonds on the "open market" from the bond dealers. The bonds then become the "reserves" that the banking establishment uses to back its loans. In another bit of sleight of hand known as "fractional reserve" lending, the same reserves are lent many times over, further expanding the money supply, generating interest for the banks with each loan. It was this money-creating process that prompted Wright Patman, Chairman of the House Banking and Currency Committee in the 1960s, to call the Federal Reserve "a total money-making machine." He wrote: "When the Federal Reserve writes a check for a government bond it does exactly what any bank does, it creates money, it created money purely and simply by writing a check." 3. The Fed generates profits for its shareholders. The interest on bonds acquired with its newly-issued Federal Reserve Notes pays the Fed’s operating expenses plus a guaranteed 6% return to its banker shareholders. A mere 6% a year may not be considered a profit in the world of Wall Street high finance, but most businesses that manage to cover all their expenses and give their shareholders a guaranteed 6% return are considered "for profit" corporations. In addition to this guaranteed 6%, the banks will now be getting interest from the taxpayers on their "reserves." The basic reserve requirement set by the Federal Reserve is 10%. The website of the Federal Reserve Bank of New York explains that as money is redeposited and relent throughout the banking system, this 10% held in "reserve" can be fanned into ten times that sum in loans; that is, $10,000 in reserves becomes $100,000 in loans. Federal Reserve Statistical Release H.8 puts the total "loans and leases in bank credit" as of September 24, 2008 at $7,049 billion. Ten percent of that is $700 billion. That means we the taxpayers will be paying interest to the banks on at least $700 billion annually – this so that the banks can retain the reserves to accumulate interest on ten times that sum in loans. The banks earn these returns from the taxpayers for the privilege of having the banks’ interests protected by an all-powerful independent private central bank, even when those interests may be opposed to the taxpayers’ -- for example, when the banks use their special status as private money creators to fund speculative derivative schemes that threaten to collapse the U.S. economy. Among other special benefits, banks and other financial institutions (but not other corporations) can borrow at the low Fed funds rate of about 2%. They can then turn around and put this money into 30-year Treasury bonds at 4.5%, earning an immediate 2.5% from the taxpayers, just by virtue of their position as favored banks. A long list of banks (but not other corporations) is also now protected from the short selling that can crash the price of other stocks.

Time to Change the Statute?

According to the Fed’s website, the control Congress has over the Federal Reserve is limited to this: "[T]he Federal Reserve is subject to oversight by Congress, which periodically reviews its activities and can alter its responsibilities by statute." As we know from watching the business news, "oversight" basically means that Congress gets to see the results when it’s over. The Fed periodically reports to Congress, but the Fed doesn’t ask; it tells. The only real leverage Congress has over the Fed is that it "can alter its responsibilities by statute." It is time for Congress to exercise that leverage and make the Federal Reserve a truly federal agency, acting by and for the people through their elected representatives. If the Fed can demand AIG’s stock in return for an $85 billion loan to the mega-insurer, we can demand the Fed’s stock in return for the trillion-or-so dollars we’ll be advancing to bail out the private banking system from its follies. If the Fed were actually a federal agency, the government could issue U.S. legal tender directly, avoiding an unnecessary interest-bearing debt to private middlemen who create the money out of thin air themselves. Among other benefits to the taxpayers. a truly "federal" Federal Reserve could lend the full faith and credit of the United States to state and local governments interest-free, cutting the cost of infrastructure in half, restoring the thriving local economies of earlier decades. Most Americans do not understand what the Federal Reserve is or why it is at the heart of our economic problems. When Americans get into discussions about the economy, most of them still blame either the Democrats or the Republicans for inflation, for the housing crash, for our rampant unemployment and for the national debt. But the truth is that the institution with the most power over our economic system is the Federal Reserve. So exactly what is the Federal Reserve? Most people would say that it is an agency of the federal government. But that is absolutely not true. In fact, the Federal Reserve itself has argued in court that it is not an agency of the federal government. Rather, the Federal Reserve is a privately-owned banking cartel that has been given a perpetual monopoly over our monetary system by the U.S. Congress. This privately-owned central bank has been destroying the value of the U.S. dollar for decades, it has run our economy into the ground and it has driven the U.S. government to the brink of bankruptcy. The Federal Reserve operates in great secrecy, it has never been subjected to a comprehensive audit and it is not accountable to the American people. Yet the decisions that the Federal Reserve makes have a dramatic impact on the lives of every single American citizen. If you really want to understand what is causing our economic problems, it is absolutely crucial that you understand exactly what the Federal Reserve system is and how it is systematically destroying our economy. Once you understand the truth about the Federal Reserve, you will view economic issues a whole lot differently. The following are 19 reasons why the Federal Reserve is at the very heart of our economic problems….

#1 The Federal Reserve system is a debt-based financial system. The way our system is designed, normally no money comes into existence without more debt being created. But this creates a huge problem, because when a new dollar is created, the interest owed to the banking system on that dollar is not also created at the same time. Therefore, the amount money that is created is not equal to the larger amount of debt that is also created. This is a Ponzi scheme that is designed to drain wealth from the American people and transfer it to the banking system. Today, the amount of debt in our economic system is far, far, far greater than the total amount of money. The only way to keep the game going is to create even more money which creates even more debt.

#2 The Federal Reserve and the bankers have a monopoly on the creation of this debt-based money. In the United States today, the only people that can create money are the bankers. You cannot create money. You would go to jail if you tried. Even the U.S. government cannot create money. Although the U.S. Constitution specifically gives Congress the power to create money, the U.S. Congress has given that power to the Federal Reserve and to the banking system. This gives them an enormous amount of power. So how does money creation actually work? Most Americans don’t understand this. As I have written about previously, the way our system is designed is that all money is supposed to originally come into existence as government debt….

Once “Federal Reserve Notes” are in circulation, there is another way that money is created. It is called “fractional reserve lending”. Once you or I deposit money into a bank, the bank is only required to keep a very small amount of it actually in the bank. The rest of it the bank can loan out to others (at interest of course). This process can be repeated over and over and over, creating more money and an even larger amount of debt. But the important part to take away from all this is that normally money is only created when debt is created, and the amount of debt to be paid back is always larger than the amount of money created. This entire system is designed to drain our wealth and to put it into the hands of the bankers.

#3 The power of money creation and debt creation is in the hands of private individuals – not the government. The Federal Reserve claims that it is an “entity within the government, having both public purposes and private aspects.” That sounds so reasonable, but the truth is that the Federal Reserve is a legalized banking cartel that is privately-owned. In fact, the Federal Reserve is about as “federal” as Federal Express is. In defending itself against a Bloomberg request for information under the Freedom of Information Act, the Federal Reserve objected by declaring that it was “not an agency” of the U.S. government and therefore it was not subject to the Freedom of Information Act. It is kind of funny how Fed officials are always talking about how important their “independence” is, but whenever anyone starts criticizing them for being private they start stressing their ties with the government. So who owns the Federal Reserve? As the Federal Reserve’s own website describes, it is the member banks that own it….

In particular, as we will see below, the banks of the New York Federal Reserve have the most influence over the system. So who owns the member banks? Well, when you trace the ownership of the member banks to the very top you find that the international banking elite are very strongly represented.

#4 The Federal Reserve itself is not much of a profit-making institution. Rather, it is a tool that enables others to make obscene amounts of money. There are many that think of the Federal Reserve as an evil profit-making machine. But the truth is that the Fed doesn’t make that much money. Rather, the system was set up so that others could make an obscene amount of money from U.S. government debt. Many of those opposed to the Federal Reserve point to the record $80.9 billion in profits that the Federal Reserve made last year as evidence that they are robbing the American people blind. But then those defending the Federal Reserve will point out that the Fed returned $78.4 billion to the U.S. Treasury. In the end, those numbers are not nearly as important as the hundreds of billions of dollars in interest that are made off of U.S. government debt each year. If the U.S. government had been issuing debt-free money all this time, the U.S. government would likely not be spending one penny on interest payments. Instead, the U.S. government spent over 413 billion dollars on interest on the national debt during fiscal 2010. This is money that belonged to U.S. taxpayers that was transferred to the U.S. government which in turn was transferred to wealthy international bankers and other foreign governments. This is where the magic of the Federal Reserve system is. It is in getting the U.S. government enslaved to debt and using that debt to transfer hundreds of billions of dollars of our wealth into the hands of others. As interest rates go up, this phenomenon is going to become even more brutal. Right now it is being projected that the U.S. government will be paying 900 billion dollars just in interest on the national debt by the year 2019. As you fill out your tax return this year, just keep in mind that vast quantities of our money is going to pay interest on debt that the U.S. government never needed to become enslaved to. There are some very happy people out there that are becoming fabulously wealthy at our expense. What a system, eh?

#5 The Federal Reserve is a perpetual debt machine. As mentioned above, the U.S. government is enslaved to debt. So how did it get enslaved? Well, instead of printing up and spending the money that it needs, the U.S. government borrows it through the Federal Reserve system at interest. In fact, as noted above, the U.S. government cannot create a single new dollar without borrowing it. But each new dollar that the U.S. government borrows creates more than a dollar of new debt. As a result, the government eventually has to collect more in taxes than what it has borrowed. This phenomenon creates an endless debt spiral. And is that not what we have in the United States today? In fact, you see this in almost every nation on earth where a similar central banking system has been established. Did you know that the U.S. national debt is more than 5,000 times larger than it was 100 years ago? That’s right – back in 1910, prior to the passage of the Federal Reserve Act, the national debt was only about $2.6 billion. The only way that the U.S. government can inject more money into the economy is by going into more debt. But when new government debt is created, the amount of money to pay the interest on that debt is not also created. In this way, it was intended by the international bankers that U.S. government debt would expand indefinitely and the U.S. money supply would also expand indefinitely. In the process, the international bankers would become insanely wealthy by lending money to the U.S. government. However, things did not have to turn out this way. If the Federal Reserve had never been created, and the U.S. government had been issuing debt-free currency all this time, it is entirely conceivable that we would have absolutely no federal government debt at this point. Unfortunately, we are now trapped in a debt-based system. The U.S. national debt simply cannot ever be paid off. U.S. government debt has been mathematically designed to expand forever. It is a trap from which there is no escape. Sadly, we have now gotten to a terminal phase of the debt spiral. The Congressional Budget Office is projecting that U.S. government debt held by the public will reach a staggering 716 percent of GDP by the year 2080. Remember when I used the term “debt spiral” earlier? This is what a debt spiral looks like….

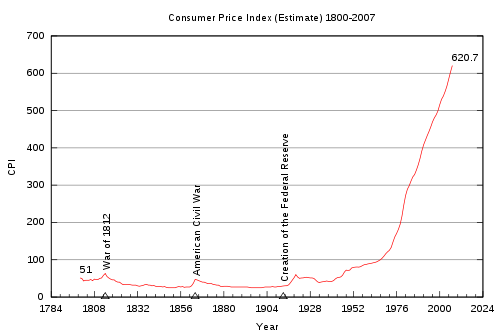

#6 The Federal Reserve system is designed to cause inflation. As U.S. government debt expands at an exponential pace, it inevitably causes inflation. Most Americans believe that inflation is a fact of life, but the truth is that the United States has only had a major, ongoing problem with inflation since the Federal Reserve was created back in 1913. Sadly, the U.S. dollar has lost well over 95 percent of its value since the Federal Reserve was created. If the Federal Reserve did not exist, it is theoretically conceivable that we could have an economy with little to no inflation. Of course that would greatly depend on the discipline of our government officials (which is not very great at this point), but the sad truth is that our current system is always going to produce inflation. In fact, the Federal Reserve system was originally designed to be inflationary. Just check out the inflation chart posted below. The U.S. never had massive problems with inflation before the Fed was created, but now it is just wildly out of control….

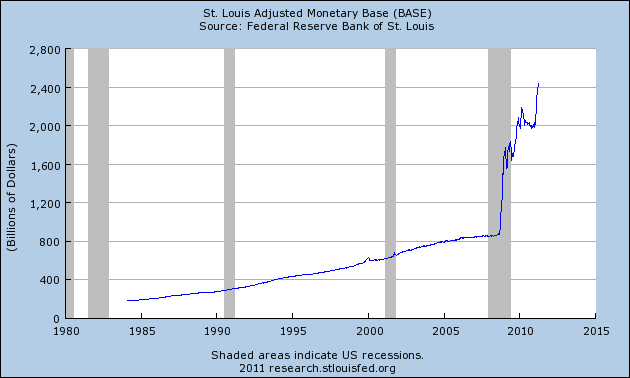

#7 The Federal Reserve has decided to play bizarre games with our money supply. In a desperate attempt to revive the dying U.S. economy, the Federal Reserve has resorted to chucking gigantic quantities of cash into the financial system. Remember how earlier I explained that normally whenever new money is created that more debt is created? Well, lately the Fed has been resorting to a trick called “quantitative easing”. What “quantitative easing” means is that the Federal Reserve zaps massive amounts of money into existence out of thin air and starts spending it on anything that it wants to buy. Lately, this has primarily been done to buy up U.S. government debt. But isn’t that “monetizing the debt”? Of course it is, and it is a blatant Ponzi scheme. However, what is even more alarming is what this is doing to our money supply. Just look at what has happened to our monetary base since about mid-2008….

Does anyone in their right mind believe that this is not going to cause horrible inflation? Right now most of the new cash is tied up in the financial system, but once it gets out into the regular economy watch out!

#8 The Federal Reserve is undemocratic. In a previous article, I asked the following question:

In both cases, a bunch of unelected elitists run the economy and make important economic decisions for the rest of us. So what really is the difference?

#9 The Federal Reserve runs the U.S. economy. Most Americans want to blame Obama or Bush or the U.S. Congress for the state of the economy. But the truth is that it is the Federal Reserve that sets interest rates, it is the Federal Reserve that determines the money supply, it is the Federal Reserve that sets the “target rate” of inflation, it is the Federal Reserve that determines if unemployment is too high or too low and it is the Federal Reserve that watches over all of our banks. Yes, Obama, Bush and the U.S. Congress all have things to answer for as well. But none of them have the direct power over the economy that the Federal Reserve does.

#10 The Federal Reserve favors the big banks. Not all financial institutions are treated equally by the Fed. The truth is that the big banks (particularly those on Wall Street) are treated with great favor by the Federal Reserve. If the Federal Reserve did not exist, the big Wall Street banks would not have such an overwhelming advantage. Most Americans simply have no idea that over the last several years the Federal Reserve has been giving gigantic piles of nearly interest-free money to the big Wall Street banks which they turned right around and started lending to the federal government at a much higher rate of return. I don’t know about you, but if I was allowed to do that I could make a whole bunch of money very quickly. In fact, it has come out that the Federal Reserve made over $9 trillion in overnight loans to major banks, large financial institutions and other “friends” during the financial crisis of 2008 and 2009. Wouldn’t you like to be able to zap trillions of dollars into existence and loan it out to your friends at very favorable terms? Sadly, most of the “help” from the Federal Reserve always seems to go to the big boys. When “small enough to fail” banks need assistance, they are usually told to go sell themselves to one of the big banks.

#11 The worse the debt problems caused by the Federal Reserve become, the more money the IRS needs to collect from the rest of us. If the U.S. government could issue debt-free money, it is conceivable that we would not even need the IRS. You doubt this? Well, the truth is that the United States did just fine for well over a hundred years without a national income tax. But about the same time the Federal Reserve was created a national income tax was instituted as well. The whole idea was that the wealth of the American people would be transferred to the U.S. government by force and then transferred into the hands of the ultra-wealthy in the form of interest payments. If the Federal Reserve was shut down, it is entirely possible that we would be able to shut down the IRS as well. But the only way that the current system works is if massive amounts of wealth continue to be drained from the American people.

#12 The Federal Reserve creates artificial financial bubbles. When you look back over the last several decades, you will find financial bubble after financial bubble. So who created all of those bubbles? It was the Federal Reserve. The ridiculous policies of Greenspan and Bernanke have wrought disaster after disaster and yet most of our politicians still will not even consider major changes to the Federal Reserve.

#13 The Federal Reserve is anti-free market. In a true free market system, the marketplace would determine what interest rates are. In a true free market system, the marketplace would determine which financial institutions survive. In a true free market system, artificial financial bubbles would be far less likely. But we don’t have a true free market system.

#14 The Federal Reserve tells the rest of the our banks what to do. Most Americans don’t understand just how much power the Federal Reserve actually has over our local banks. For example, just last year Federal Reserve officials walked into one bank in Oklahoma and demanded that they take down all the Bible verses and all the Christmas buttons that the bank had been displaying.

#15 The people currently running the Federal Reserve pretty much have no idea what they are doing. In case anyone has not noticed, Federal Reserve Chairman Ben Bernanke has a very long track record of incompetence. Nearly every major judgment that he has made since taking over that position has been dead wrong. If one of us could go down the street and appoint the manager of the local Dairy Queen as the Chairman of the Federal Reserve, it is very doubtful that person would do a worse job than Bernanke has done.

#16 Even though the Federal Reserve has such extraordinary power over the financial system, the American people are not permitted to examine their books. The Federal Reserve claims that they are regularly audited, but when some members of Congress attempted to push through a true comprehensive audit of the Fed last year Federal Reserve officials threw a hissy fit. The truth is that the Federal Reserve has never undergone a true comprehensive audit since it was created back in 1913. Whenever the subject of an audit comes up, Bernanke and others at the Fed keep repeating the mantra of how important “the independence of the Federal Reserve” is. Sadly, Ron Paul’s proposal to audit the Federal Reserve last year, which had previously been co-sponsored by 320 members of the U.S. House of Representatives, ultimately failed by a vote of 229-198. Instead, a very, very limited examination of Fed transactions that occurred during the recent financial crisis was approved. So what did that limited examination reveal? Well, the Federal Reserve was forced to reveal the details of 21,000 transactions stretching from December 2007 to July 2010 that combined were worth trillions of dollars. It turns out that the Federal Reserve was just handing out gigantic piles of nearly interest-free cash to their friends at the largest banks, financial institutions and corporations all over the globe. Many members of Congress were absolutely stunned by these revelations. So what would a more comprehensive audit reveal?

#17 The Federal Reserve has way too much power. If the Federal Reserve did not exist, we would not have an unelected, unaccountable “fourth branch of government” running around that has gotten completely and totally out of control. Even some members of Congress are now openly complaining about how much power the Fed has. For example, Ron Paul told MSNBC last year that he believes that the Federal Reserve is now more powerful than Congress…..

#18 The Federal Reserve is dominated by Wall Street and the New York banks. The New York representative is the only permanent member of the Federal Open Market Committee, while other regional banks rotate in 2 and 3 year intervals. The former head of the New York Fed, Timothy Geithner, is now U.S. Treasury Secretary. The truth is that the Federal Reserve Bank of New York has always been the most important of the regional Fed banks by far, and in turn the Federal Reserve Bank of New York has always been dominated by Wall Street and the major New York banks. The cold, hard reality of the matter is that the Federal Reserve is just another one of the tools that the Wall Street banking elite use to dominate all the rest of us.

#19 The Federal Reserve has brought us to the brink of economic collapse. If the Federal Reserve had never been created, the American people would not be so enslaved to debt. At the very core of our economic problems is debt. American consumers are swamped with debt, state and local governments are facing horrific debt problems from coast to coast and the federal government has piled up the biggest mountain of debt in the history of the world. We are living in an absolutely massive debt bubble, and when it bursts the world is going to experience financial chaos like it has never seen before. Things did not have to turn out this way. We did not have to adopt a debt-based financial system. We did not have to allow the bankers to enslave us with debt. But that is what happened. Sadly, most Americans and the vast majority of our politicians are still clueless about these issues. In 1922, Henry Ford wrote the following….

Hopefully this article will help people understand our debt-based financial system a little bit better. Until we fundamentally change our system, many of the economic and financial problems we are currently experiencing will never go away. Thankfully, it does appear that some Americans are waking up. According to a recent Bloomberg National Poll, the number of Americans that would like to see the Federal Reserve held more accountable or even completely abolished is increasing….

Those are very exciting numbers. Hopefully we can awaken many more Americans to the dangers of a debt-based economy. In the book of Proverbs, it tells us the following….

Well, by allowing ourselves to become enslaved to debt, we have become the servants of the international banking system. Not only that, we have also sold our children and our grandchildren into perpetual debt slavery. Thomas Jefferson tried to warn us about this. He believed that when the government borrows money in one generation which must be paid back by future generations it is equivalent to stealing….

In fact, Thomas Jefferson said that if he could add one more amendment to the U.S. Constitution it would be a ban on all government borrowing….

Where would we be today if we had listened to Thomas Jefferson? The amount of government debt that we have racked up is a great evil. We have stolen the future away from our children and our grandchildren. We have put them in a position where they will spend the rest of their lives paying off our debts to the bankers. We owe it to future generations to fix the problems that we have created. That is why so many of us believe that it is time for the U.S. Congress to shut down the Federal Reserve. Our current financial system is a complete and utter failure and we need to start over. |

The Federal Reserve is the chief culprit behind the economic crisis. Its unchecked power to create endless amounts of money out of thin air brought us the boom and bust cycle and causes one financial bubble after another. Since the Fed’s creation in 1913 the dollar has lost more than 96% of its value, and by recklessly inflating the money supply the Fed continues to distort interest rates and intentionally erodes the value of the dollar. For the past 30 years, Congressman Ron Paul has worked tirelessly to bring much-needed transparency and accountability to the secretive bank. And in 2009 and 2010 his unfaltering dedication showed astonishing results: HR 1207, the bill to audit the Federal Reserve, swept the country and made the central bankers shudder at their desks. The bill passed as an amendment both in the House Financial Services Committee and in the House itself. But eventually the most significant portions of the bill were derailed. (Full story here.) This year, Audit the Fed is back with a vengeance. Reintroduced on 01/26/2011 as HR 459, Ron Paul’s bill to audit the Federal Reserve now has 176 co-sponsors, and the numbers keep growing! HR 459′s companion bill in the Senate, S 202, has already attracted 7 co-sponsors. This is history in the making, and victory is within reach. Imagine what will happen if HR 459, The Federal Reserve Transparency Act, comes up for vote in Congress! It has real potential to pass — BUT only if we educate and rally the people to support it and get our Congress people to put it to vote and pass it. The Four Horsemen of Banking (Bank of America, JP Morgan Chase, Citigroup and Wells Fargo) own the Four Horsemen of Oil (Exxon Mobil, Royal Dutch/Shell, BP Amoco and Chevron Texaco); in tandem with Deutsche Bank, BNP, Barclays and other European old money behemoths. But their monopoly over the global economy does not end at the edge of the oil patch. According to company 10K filings to the SEC, the Four Horsemen of Banking are among the top ten stock holders of virtually every Fortune 500 corporation.[1] So who then are the stockholders in these money center banks? This information is guarded much more closely. My queries to bank regulatory agencies regarding stock ownership in the top 25 US bank holding companies were given Freedom of Information Act status, before being denied on “national security” grounds. This is rather ironic, since many of the bank’s stockholders reside in Europe. One important repository for the wealth of the global oligarchy that owns these bank holding companies is US Trust Corporation – founded in 1853 and now owned by Bank of America. A recent US Trust Corporate Director and Honorary Trustee was Walter Rothschild. Other directors included Daniel Davison of JP Morgan Chase, Richard Tucker of Exxon Mobil, Daniel Roberts of Citigroup and Marshall Schwartz of Morgan Stanley. [2] J. W. McCallister, an oil industry insider with House of Saud connections, wrote in The Grim Reaper that information he acquired from Saudi bankers cited 80% ownership of the New York Federal Reserve Bank- by far the most powerful Fed branch- by just eight families, four of which reside in the US. They are the Goldman Sachs, Rockefellers, Lehmans and Kuhn Loebs of New York; the Rothschilds of Paris and London; the Warburgs of Hamburg; the Lazards of Paris; and the Israel Moses Seifs of Rome. CPA Thomas D. Schauf corroborates McCallister’s claims, adding that ten banks control all twelve Federal Reserve Bank branches. He names N.M. Rothschild of London, Rothschild Bank of Berlin, Warburg Bank of Hamburg, Warburg Bank of Amsterdam, Lehman Brothers of New York, Lazard Brothers of Paris, Kuhn Loeb Bank of New York, Israel Moses Seif Bank of Italy, Goldman Sachs of New York and JP Morgan Chase Bank of New York. Schauf lists William Rockefeller, Paul Warburg, Jacob Schiff and James Stillman as individuals who own large shares of the Fed. [3] The Schiffs are insiders at Kuhn Loeb. The Stillmans are Citigroup insiders, who married into the Rockefeller clan at the turn of the century. Eustace Mullins came to the same conclusions in his book The Secrets of the Federal Reserve, in which he displays charts connecting the Fed and its member banks to the families of Rothschild, Warburg, Rockefeller and the others. [4] The control that these banking families exert over the global economy cannot be overstated and is quite intentionally shrouded in secrecy. Their corporate media arm is quick to discredit any information exposing this private central banking cartel as “conspiracy theory”. Yet the facts remain. The House of MorganThe Federal Reserve Bank was born in 1913, the same year US banking scion J. Pierpont Morgan died and the Rockefeller Foundation was formed. The House of Morgan presided over American finance from the corner of Wall Street and Broad, acting as quasi-US central bank since 1838, when George Peabody founded it in London. Peabody was a business associate of the Rothschilds. In 1952 Fed researcher Eustace Mullins put forth the supposition that the Morgans were nothing more than Rothschild agents. Mullins wrote that the Rothschilds, “…preferred to operate anonymously in the US behind the facade of J.P. Morgan & Company”. [5] Author Gabriel Kolko stated, “Morgan’s activities in 1895-1896 in selling US gold bonds in Europe were based on an alliance with the House of Rothschild.” [6] The Morgan financial octopus wrapped its tentacles quickly around the globe. Morgan Grenfell operated in London. Morgan et Ce ruled Paris. The Rothschild’s Lambert cousins set up Drexel & Company in Philadelphia. The House of Morgan catered to the Astors, DuPonts, Guggenheims, Vanderbilts and Rockefellers. It financed the launch of AT&T, General Motors, General Electric and DuPont. Like the London-based Rothschild and Barings banks, Morgan became part of the power structure in many countries. By 1890 the House of Morgan was lending to Egypt’s central bank, financing Russian railroads, floating Brazilian provincial government bonds and funding Argentine public works projects. A recession in 1893 enhanced Morgan’s power. That year Morgan saved the US government from a bank panic, forming a syndicate to prop up government reserves with a shipment of $62 million worth of Rothschild gold. [7] Morgan was the driving force behind Western expansion in the US, financing and controlling West-bound railroads through voting trusts. In 1879 Cornelius Vanderbilt’s Morgan-financed New York Central Railroad gave preferential shipping rates to John D. Rockefeller’s budding Standard Oil monopoly, cementing the Rockefeller/Morgan relationship. The House of Morgan now fell under Rothschild and Rockefeller family control. A New York Herald headline read, “Railroad Kings Form Gigantic Trust”. J. Pierpont Morgan, who once stated, “Competition is a sin”, now opined gleefully, “Think of it. All competing railroad traffic west of St. Louis placed in the control of about thirty men.”[8] Morgan and Edward Harriman’s banker Kuhn Loeb held a monopoly over the railroads, while banking dynasties Lehman, Goldman Sachs and Lazard joined the Rockefellers in controlling the US industrial base. [9] In 1903 Banker’s Trust was set up by the Eight Families. Benjamin Strong of Banker’s Trust was the first Governor of the New York Federal Reserve Bank. The 1913 creation of the Fed fused the power of the Eight Families to the military and diplomatic might of the US government. If their overseas loans went unpaid, the oligarchs could now deploy US Marines to collect the debts. Morgan, Chase and Citibank formed an international lending syndicate. The House of Morgan was cozy with the British House of Windsor and the Italian House of Savoy. The Kuhn Loebs, Warburgs, Lehmans, Lazards, Israel Moses Seifs and Goldman Sachs also had close ties to European royalty. By 1895 Morgan controlled the flow of gold in and out of the US. The first American wave of mergers was in its infancy and was being promoted by the bankers. In 1897 there were sixty-nine industrial mergers. By 1899 there were twelve-hundred. In 1904 John Moody – founder of Moody’s Investor Services – said it was impossible to talk of Rockefeller and Morgan interests as separate. [10] Public distrust of the combine spread. Many considered them traitors working for European old money. Rockefeller’s Standard Oil, Andrew Carnegie’s US Steel and Edward Harriman’s railroads were all financed by banker Jacob Schiff at Kuhn Loeb, who worked closely with the European Rothschilds. Several Western states banned the bankers. Populist preacher William Jennings Bryan was thrice the Democratic nominee for President from 1896 -1908. The central theme of his anti-imperialist campaign was that America was falling into a trap of “financial servitude to British capital”. Teddy Roosevelt defeated Bryan in 1908, but was forced by this spreading populist wildfire to enact the Sherman Anti-Trust Act. He then went after the Standard Oil Trust. In 1912 the Pujo hearings were held, addressing concentration of power on Wall Street. That same year Mrs. Edward Harriman sold her substantial shares in New York’s Guaranty Trust Bank to J.P. Morgan, creating Morgan Guaranty Trust. Judge Louis Brandeis convinced President Woodrow Wilson to call for an end to interlocking board directorates. In 1914 the Clayton Anti-Trust Act was passed. Jack Morgan – J. Pierpont’s son and successor – responded by calling on Morgan clients Remington and Winchester to increase arms production. He argued that the US needed to enter WWI. Goaded by the Carnegie Foundation and other oligarchy fronts, Wilson accommodated. As Charles Tansill wrote in America Goes to War, “Even before the clash of arms, the French firm of Rothschild Freres cabled to Morgan & Company in New York suggesting the flotation of a loan of $100 million, a substantial part of which was to be left in the US to pay for French purchases of American goods.” The House of Morgan financed half the US war effort, while receiving commissions for lining up contractors like GE, Du Pont, US Steel, Kennecott and ASARCO. All were Morgan clients. Morgan also financed the British Boer War in South Africa and the Franco-Prussian War. The 1919 Paris Peace Conference was presided over by Morgan, which led both German and Allied reconstruction efforts. [11] In the 1930’s populism resurfaced in America after Goldman Sachs, Lehman Bank and others profited from the Crash of 1929. [12] House Banking Committee Chairman Louis McFadden (D-NY) said of the Great Depression, “It was no accident. It was a carefully contrived occurrence…The international bankers sought to bring about a condition of despair here so they might emerge as rulers of us all”. Sen. Gerald Nye (D-ND) chaired a munitions investigation in 1936. Nye concluded that the House of Morgan had plunged the US into WWI to protect loans and create a booming arms industry. Nye later produced a document titled The Next War, which cynically referred to “the old goddess of democracy trick”, through which Japan could be used to lure the US into WWII. In 1937 Interior Secretary Harold Ickes warned of the influence of “America’s 60 Families”. Historian Ferdinand Lundberg later penned a book of the exact same title. Supreme Court Justice William O. Douglas decried, “Morgan influence…the most pernicious one in industry and finance today.” Jack Morgan responded by nudging the US towards WWII. Morgan had close relations with the Iwasaki and Dan families – Japan’s two wealthiest clans – who have owned Mitsubishi and Mitsui, respectively, since the companies emerged from 17th Century shogunates. When Japan invaded Manchuria, slaughtering Chinese peasants at Nanking, Morgan downplayed the incident. Morgan also had close relations with Italian fascist Benito Mussolini, while German Nazi Dr. Hjalmer Schacht was a Morgan Bank liaison during WWII. After the war Morgan representatives met with Schacht at the Bank of International Settlements (BIS) in Basel, Switzerland. [13] The House of RockefellerBIS is the most powerful bank in the world, a global central bank for the Eight Families who control the private central banks of almost all Western and developing nations. The first President of BIS was Rockefeller banker Gates McGarrah- an official at Chase Manhattan and the Federal Reserve. McGarrah was the grandfather of former CIA director Richard Helms. The Rockefellers- like the Morgans- had close ties to London. David Icke writes in Children of the Matrix, that the Rockefellers and Morgans were just “gofers” for the European Rothschilds. [14] BIS is owned by the Federal Reserve, Bank of England, Bank of Italy, Bank of Canada, Swiss National Bank, Nederlandsche Bank, Bundesbank and Bank of France. Historian Carroll Quigley wrote in his epic book Tragedy and Hope that BIS was part of a plan, “to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole…to be controlled in a feudalistic fashion by the central banks of the world acting in concert by secret agreements.” The US government had a historical distrust of BIS, lobbying unsuccessfully for its demise at the 1944 post-WWII Bretton Woods Conference. Instead the Eight Families’ power was exacerbated, with the Bretton Woods creation of the IMF and the World Bank. The US Federal Reserve only took shares in BIS in September 1994. [15] BIS holds at least 10% of monetary reserves for at least 80 of the world’s central banks, the IMF and other multilateral institutions. It serves as financial agent for international agreements, collects information on the global economy and serves as lender of last resort to prevent global financial collapse. BIS promotes an agenda of monopoly capitalist fascism. It gave a bridge loan to Hungary in the 1990’s to ensure privatization of that country’s economy. It served as conduit for Eight Families funding of Adolf Hitler- led by the Warburg’s J. Henry Schroeder and Mendelsohn Bank of Amsterdam. Many researchers assert that BIS is at the nadir of global drug money laundering. [16] It is no coincidence that BIS is headquartered in Switzerland, favorite hiding place for the wealth of the global aristocracy and headquarters for the P-2 Italian Freemason’s Alpina Lodge and Nazi International. Other institutions which the Eight Families control include the World Economic Forum, the International Monetary Conference and the World Trade Organization. Bretton Woods was a boon to the Eight Families. The IMF and World Bank were central to this “new world order”. In 1944 the first World Bank bonds were floated by Morgan Stanley and First Boston. The French Lazard family became more involved in House of Morgan interests. Lazard Freres- France’s biggest investment bank- is owned by the Lazard and David-Weill families- old Genoese banking scions represented by Michelle Davive. A recent Chairman and CEO of Citigroup was Sanford Weill. In 1968 Morgan Guaranty launched Euro-Clear, a Brussels-based bank clearing system for Eurodollar securities. It was the first such automated endeavor. Some took to calling Euro-Clear “The Beast”. Brussels serves as headquarters for the new European Central Bank and for NATO. In 1973 Morgan officials met secretly in Bermuda to illegally resurrect the old House of Morgan, twenty years before Glass Steagal Act was repealed. Morgan and the Rockefellers provided the financial backing for Merrill Lynch, boosting it into the Big 5 of US investment banking. Merrill is now part of Bank of America. John D. Rockefeller used his oil wealth to acquire Equitable Trust, which had gobbled up several large banks and corporations by the 1920’s. The Great Depression helped consolidate Rockefeller’s power. His Chase Bank merged with Kuhn Loeb’s Manhattan Bank to form Chase Manhattan, cementing a long-time family relationship. The Kuhn-Loeb’s had financed – along with Rothschilds – Rockefeller’s quest to become king of the oil patch. National City Bank of Cleveland provided John D. with the money needed to embark upon his monopolization of the US oil industry. The bank was identified in Congressional hearings as being one of three Rothschild-owned banks in the US during the 1870’s, when Rockefeller first incorporated as Standard Oil of Ohio. [17] One Rockefeller Standard Oil partner was Edward Harkness, whose family came to control Chemical Bank. Another was James Stillman, whose family controlled Manufacturers Hanover Trust. Both banks have merged under the JP Morgan Chase umbrella. Two of James Stillman’s daughters married two of William Rockefeller’s sons. The two families control a big chunk of Citigroup as well. [18] In the insurance business, the Rockefellers control Metropolitan Life, Equitable Life, Prudential and New York Life. Rockefeller banks control 25% of all assets of the 50 largest US commercial banks and 30% of all assets of the 50 largest insurance companies. [19] Insurance companies- the first in the US was launched by Freemasons through their Woodman’s of America- play a key role in the Bermuda drug money shuffle. Companies under Rockefeller control include Exxon Mobil, Chevron Texaco, BP Amoco, Marathon Oil, Freeport McMoran, Quaker Oats, ASARCO, United, Delta, Northwest, ITT, International Harvester, Xerox, Boeing, Westinghouse, Hewlett-Packard, Honeywell, International Paper, Pfizer, Motorola, Monsanto, Union Carbide and General Foods. The Rockefeller Foundation has close financial ties to both Ford and Carnegie Foundations. Other family philanthropic endeavors include Rockefeller Brothers Fund, Rockefeller Institute for Medical Research, General Education Board, Rockefeller University and the University of Chicago- which churns out a steady stream of far right economists as apologists for international capital, including Milton Friedman. The family owns 30 Rockefeller Plaza, where the national Christmas tree is lighted every year, and Rockefeller Center. David Rockefeller was instrumental in the construction of the World Trade Center towers. The main Rockefeller family home is a hulking complex in upstate New York known as Pocantico Hills. They also own a 32-room 5th Avenue duplex in Manhattan, a mansion in Washington, DC, Monte Sacro Ranch in Venezuela, coffee plantations in Ecuador, several farms in Brazil, an estate at Seal Harbor, Maine and resorts in the Caribbean, Hawaii and Puerto Rico. [20] The Dulles and Rockefeller families are cousins. Allen Dulles created the CIA, assisted the Nazis, covered up the Kennedy hit from his Warren Commission perch and struck a deal with the Muslim Brotherhood to create mind-controlled assassins. [21] Brother John Foster Dulles presided over the phony Goldman Sachs trusts before the 1929 stock market crash and helped his brother overthrow governments in Iran and Guatemala. Both were Skull & Bones, Council on Foreign Relations (CFR) insiders and 33rd Degree Masons. [22] The Rockefellers were instrumental in forming the depopulation-oriented Club of Rome at their family estate in Bellagio, Italy. Their Pocantico Hills estate gave birth to the Trilateral Commission. The family is a major funder of the eugenics movement which spawned Hitler, human cloning and the current DNA obsession in US scientific circles. John Rockefeller Jr. headed the Population Council until his death. [23] His namesake son is a Senator from West Virginia. Brother Winthrop Rockefeller was Lieutenant Governor of Arkansas and remains the most powerful man in that state. In an October 1975 interview with Playboy magazine, Vice-President Nelson Rockefeller- who was also Governor of New York- articulated his family’s patronizing worldview, “I am a great believer in planning- economic, social, political, military, total world planning.” But of all the Rockefeller brothers, it is Trilateral Commission (TC) founder and Chase Manhattan Chairman David who has spearheaded the family’s fascist agenda on a global scale. He defended the Shah of Iran, the South African apartheid regime and the Chilean Pinochet junta. He was the biggest financier of the CFR, the TC and (during the Vietnam War) the Committee for an Effective and Durable Peace in Asia- a contract bonanza for those who made their living off the conflict. Nixon asked him to be Secretary of Treasury, but Rockefeller declined the job, knowing his power was much greater at the helm of the Chase. Author Gary Allen writes in The Rockefeller File that in 1973, “David Rockefeller met with twenty-seven heads of state, including the rulers of Russia and Red China.” Following the 1975 Nugan Hand Bank/CIA coup against Australian Prime Minister Gough Whitlam, his British Crown-appointed successor Malcolm Fraser sped to the US, where he met with President Gerald Ford after conferring with David Rockefeller. |

In early 2011, Rep. Ron Paul introduced H.R. 459, the “The Federal Reserve Transparency Act of 2011.” This is a new version of the broader audit bill he and others were looking for back in 2010. Rep. Paul’s remarks while introducing the measure in early 2011 can be read

In early 2011, Rep. Ron Paul introduced H.R. 459, the “The Federal Reserve Transparency Act of 2011.” This is a new version of the broader audit bill he and others were looking for back in 2010. Rep. Paul’s remarks while introducing the measure in early 2011 can be read

No comments:

Post a Comment